How FHA Home Loans Make Homeownership A Lot More Available

Wiki Article

Exploring Home Loans: How Diverse Funding Programs Can Assist You Attain Your Imagine Homeownership

Browsing the landscape of mortgage discloses a variety of programs developed to accommodate different economic scenarios, inevitably promoting the trip to homeownership. From FHA fundings that supply reduced down payment alternatives to VA finances that forgo deposit demands for eligible veterans, the choices can seem frustrating yet appealing. In addition, traditional lendings offer customized options for those with distinct credit report profiles, while specialized programs sustain newbie buyers. As we check out these varied finance alternatives, it ends up being clear that understanding their ins and outs is vital for making well-informed choices in your quest of a home.Kinds Of Home Mortgage Programs

When considering financing options for acquiring a home, it is necessary to understand the various sorts of home finance programs available. Each program is developed to cater to various purchaser circumstances, monetary scenarios, and home types, giving possible home owners with a variety of choices.Traditional finances, generally used by personal lenders, are one of one of the most common options. These lendings are not insured or ensured by the federal government and might call for a higher credit rating rating and a larger down settlement. On the other hand, government-backed finances, such as those from the Federal Real Estate Management (FHA), Department of Veterans Matters (VA), and the U.S. Department of Farming (USDA), give even more adaptable credentials and reduced deposit alternatives.

Adjustable-rate home loans (ARMs) use rates of interest that can change in time, providing lower preliminary repayments yet potentially raising prices in the future. Fixed-rate mortgages, on the various other hand, keep a consistent interest price throughout the finance term, giving stability in month-to-month repayments. Comprehending these different financing programs is important for potential property owners to make enlightened decisions that align with their monetary goals and homeownership desires.

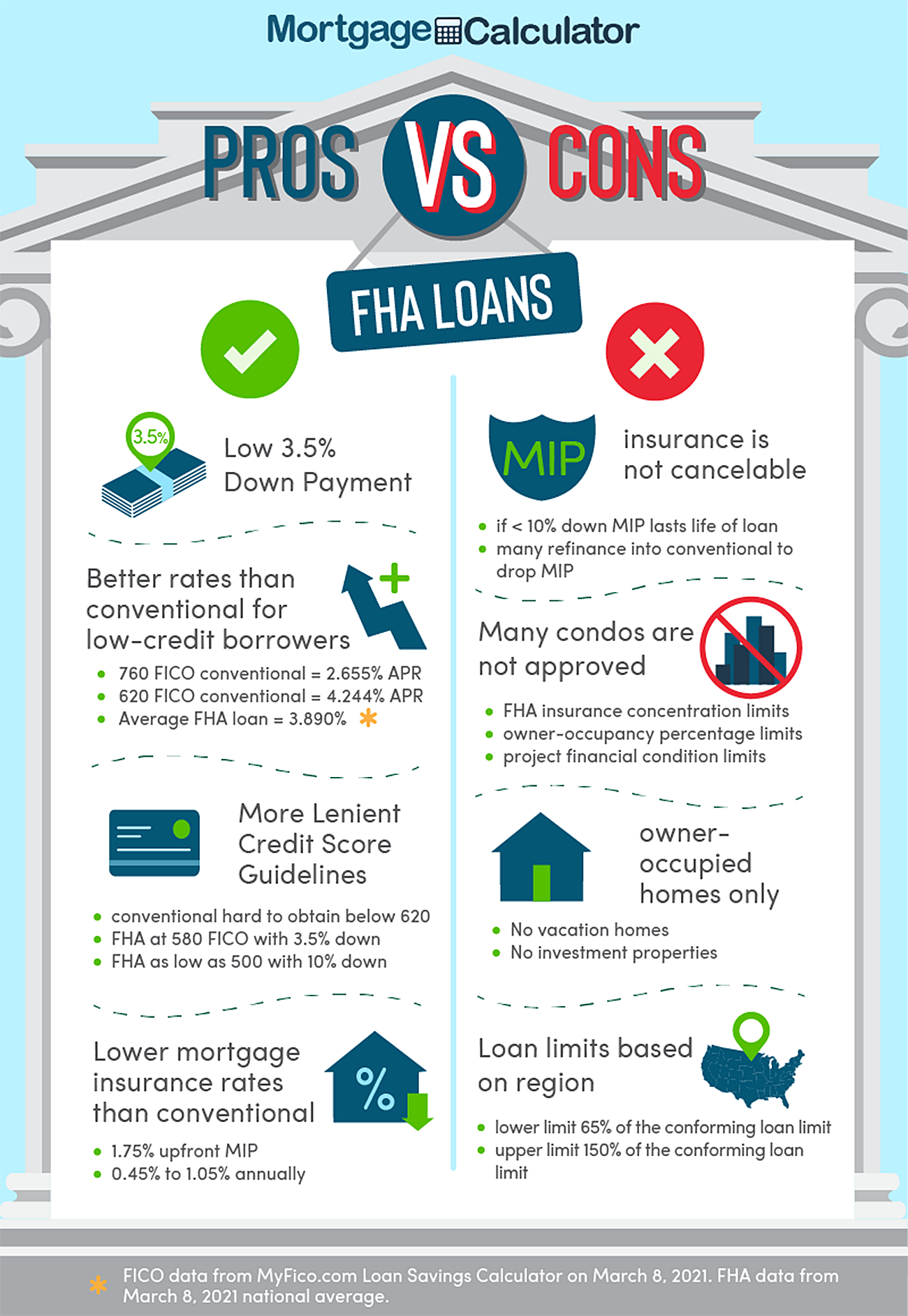

Benefits of FHA Fundings

FHA financings provide many benefits that make them an eye-catching option for several homebuyers, specifically newbie buyers. One of the primary benefits is the reduced down settlement need, which can be as reduced as 3.5% of the acquisition rate. This dramatically minimizes the in advance monetary problem for buyers who might be struggling to save for a traditional deposit.Another benefit is the flexibility in credit history requirements. FHA car loans allow for reduced credit report contrasted to conventional loans, enabling people with less-than-perfect credit to receive financing (FHA home loans). Furthermore, FHA lendings are assumable, indicating that if you sell your home, the purchaser can take control of your funding under the existing terms, which can be a selling point in an affordable market

FHA loans likewise provide competitive rate of interest, which can lead to lower monthly settlements gradually. Moreover, these finances are backed by the Federal Housing Administration, supplying a degree of safety and security for lending institutions that may encourage them to provide a lot more desirable terms to customers.

Comprehending VA Loans

The special benefits of VA financings make them an engaging choice for qualified veterans and active-duty solution participants seeking to purchase a home. Designed particularly to recognize army solution, these financings use a number of key benefits that can significantly alleviate the home-buying process. One of one of the most remarkable benefits is the absence of a down settlement requirement, which enables experts to safeguard funding without the normal obstacles that numerous newbie property buyers encounter.In addition, VA loans do not call for exclusive mortgage insurance policy (PMI), more making and minimizing month-to-month settlements homeownership extra cost effective. The passion prices related to VA lendings are often less than those of conventional finances, which can bring about substantial savings over the life of the home mortgage.

In addition, VA lendings come with flexible credit history needs, making them obtainable to a more comprehensive variety of candidates. Overall, VA fundings stand for a valuable resource for those that have offered in the army, facilitating their desires of homeownership with positive terms and problems.

Standard Car Loan Choices

Flexibility is a hallmark of conventional car loan options, which deal with a wide variety of customers in the home-buying procedure. These fundings are not backed by any kind of government firm, making them a popular click for source option for those looking for even more customized lending options. Standard loans normally come in two kinds: adjusting and non-conforming. Conforming fundings abide by the guidelines set by Fannie Mae and Freddie Mac, that include finance limits and debtor credit rating needs. In contrast, non-conforming lendings might surpass these limitations and are often sought by high-net-worth individuals or those with unique financial scenarios.

Conventional loans generally need a down repayment varying from 3% to 20%, depending upon the lender and the consumer's credit rating account. Furthermore, personal home mortgage insurance policy (PMI) may be required for deposits listed below 20%, making certain that consumers have numerous pathways to homeownership.

Specialized Funding Programs

Many consumers discover that specialized car loan programs can provide tailored solutions to satisfy their distinct monetary scenarios and homeownership goals. These programs are made to resolve particular needs that standard financings might not properly meet. First-time homebuyers can profit from programs supplying down repayment aid or decreased mortgage insurance premiums, making homeownership more achievable.Veterans and active-duty military personnel might discover VA loans, which supply affordable rate of interest and the advantage of no down repayment. In a similar way, USDA lendings provide to country buyers, providing funding options with minimal down settlement demands for eligible homes.

In addition, specialized loan programs can sustain buyers with reduced credit report scores with FHA finances, which are backed by the Federal Real Estate Management. These loans often come with even more adaptable certification needs, enabling consumers to protect funding in spite of monetary difficulties.

Conclusion

In verdict, the varied range of home mortgage programs offered provides vital assistance for people desiring accomplish homeownership. Programs such as FHA fundings, VA loans, and traditional choices satisfy different monetary circumstances and needs. Specialized finance initiatives additionally help specific teams, consisting of new customers and those with lower credit rating. Understanding these options enables potential home owners to browse the complexities of funding, ultimately assisting in educated choices and enhancing the chance of successful homeownership.From FHA lendings that provide lower down helpful resources repayment options to VA fundings that forgo down repayment demands for qualified experts, the options can seem overwhelming yet encouraging. FHA finances permit for lower credit ratings compared to standard financings, making it possible for individuals with less-than-perfect credit report to qualify for funding. In addition, FHA lendings are assumable, implying that if you offer your home, the buyer can take over your loan my explanation under the existing terms, which can be a selling point in a competitive market.

Adhering car loans stick to the guidelines set by Fannie Mae and Freddie Mac, which consist of lending restrictions and customer credit score demands. Programs such as FHA fundings, VA car loans, and traditional choices provide to numerous economic circumstances and demands.

Report this wiki page